.png)

Service Design · DCE Strategy · JPMorgan Chase · 5,000+ internal users · 10+ touchpoints

Help one of the world's largest banks understand why millions of customers were receiving inconsistent experiences — and design the strategic framework to fix it.

I was the service designer on this initiative - working across discovery, research synthesis, stakeholder facilitation, and strategic framing. I owned the process from customer needs mapping through to executive-facing recommendations.

What I want to be clear about: this was a strategy and discovery engagement, not a shipped product. My contribution was defining what needed to be built and why - not building it. That distinction matters and I'll be honest about it throughout.

FigJam · Miro · LLM Suite· PowerPoint · Figma

Relationship managers · Business bankers · Business banking clients · Internal product, engineering, and compliance teams

Background: Why Customer Segmentation Matters in Banking

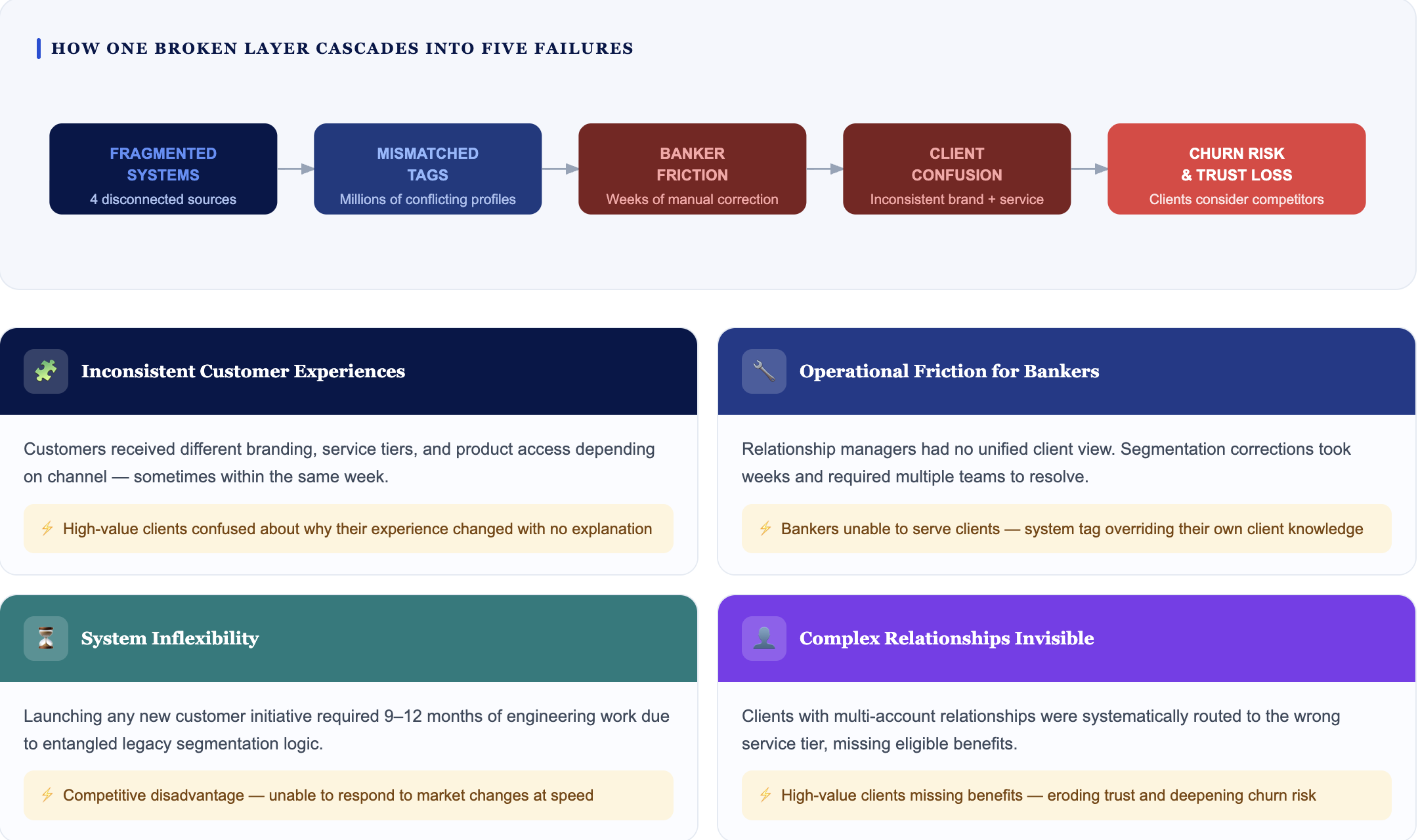

In a large financial institution like JPMC, customer segmentation is the foundational layer that determines what products, benefits, service tiers, and brand experiences each customer receives. When it works, customers get the right treatment at the right time. When it breaks - which it had in this case -the consequences cascade across every channel, every relationship, and every customer interaction.

JPMC had built multiple independent segmentation approaches over decades - one for JPMorgan Private Bank, another for Chase Private Client, another for Business Banking, another for Starters. Each made sense in isolation. Together they created three interconnected failures that no single team could see in full.

Experience Inconsistency - customers received incorrect visual branding, lost access to features they were entitled to, received the wrong service level, and experienced completely different products across web, mobile, and branch -despite being the same customer.

System Inflexibility - adding or modifying a customer segment took an unreasonably long time. Teams couldn't efficiently track downstream consumers of any change. Nobody knew the true scale of impact when something was modified.

Operational Inefficiency -no team had a comprehensive view of a customer's full relationships across accounts. Changing a customer's segment was slow, manual, and had almost no override capability.

The consequence was a customer with a Chase checking account, a JPMorgan investment account, and a business banking relationship who experienced completely different versions of their bank

"The core insight that shaped everything: this wasn't a technology problem, a data problem, or a process problem in isolation. It was a service design problem - a failure to design the end-to-end system of how customers are understood, categorised, and served across every touchpoint simultaneously."

The organisation had many people who understood pieces of the problem. Relationship managers who experienced the daily friction. Product teams who knew the system constraints. Compliance teams who owned the governance rules. Data teams who managed the segmentation logic. No one had synthesised all of those perspectives simultaneously.

My approach was a structured collaborative discovery using a customer needs canvas -mapping four dimensions across all stakeholder groups at once: who they are, what job they're trying to do, what's blocking them, and what evidence exists for that block.

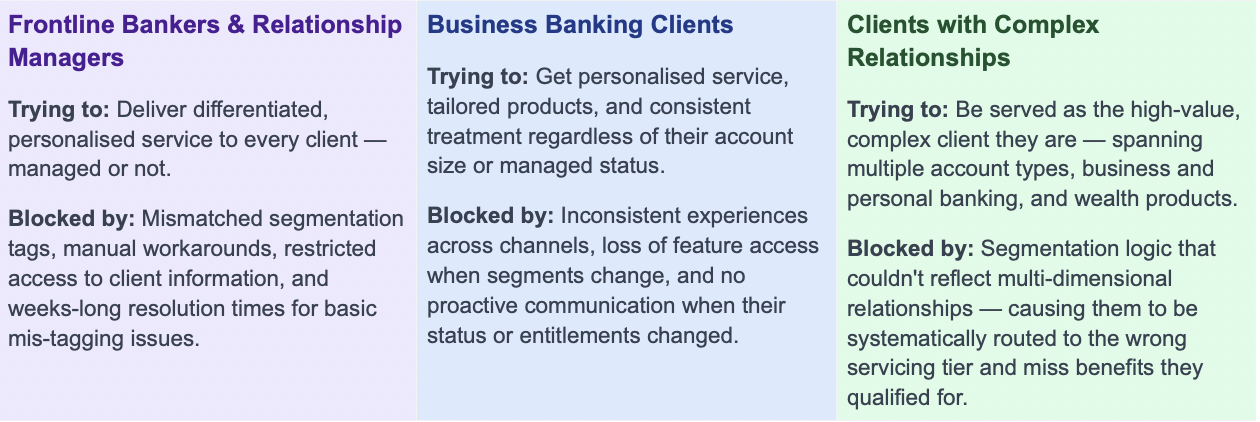

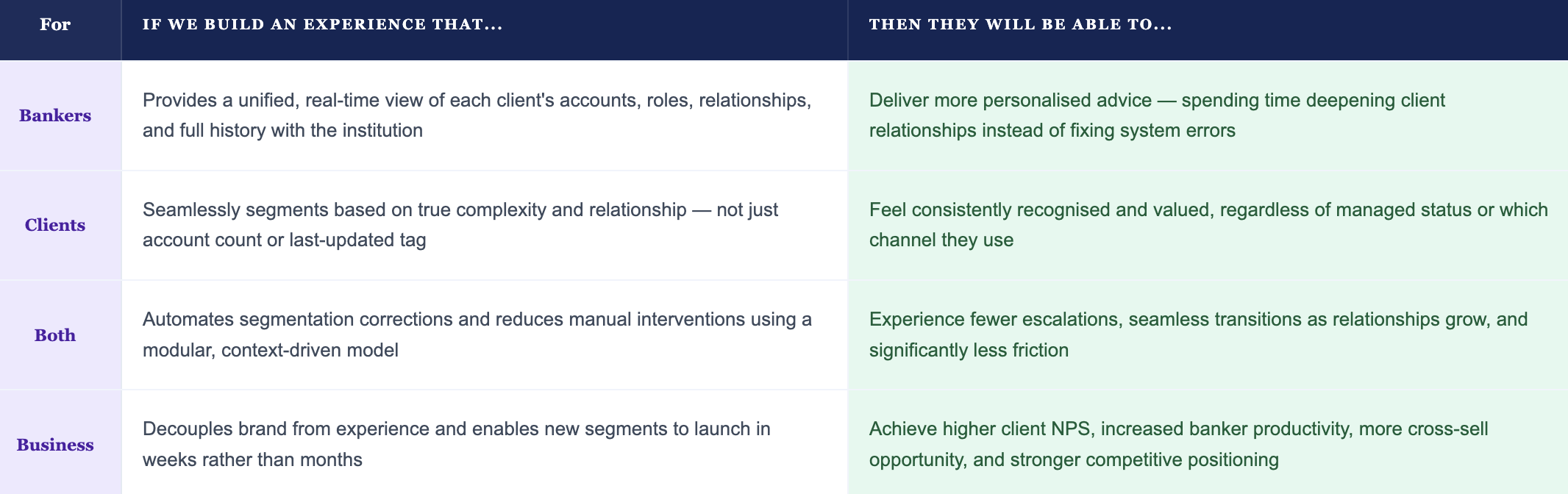

Who We Are Solving For

The discovery surfaced three distinct user groups, each experiencing the segmentation problem from a different vantage point:

What the evidence revealed - in three patterns:

Pattern 1 : Relationship friction was systemic, not isolated. Bankers consistently reported being unable to serve clients correctly because the system didn't reflect the relationship they had built. A relationship manager who knew their client had just sold a business couldn't trigger the experience upgrade that client deserved - because the segmentation system hadn't been updated and the process to update it was weeks long.

Pattern 2 : Multi-relationship customers were disproportionately affected. The more products a client held - checking, investment, business, wealth management - the more likely they were to experience inconsistency. More systems needed to be in sync. More often they weren't.

Pattern 3 : Operational costs were compounding silently. Every mis-tagging event triggered a manual correction process requiring multiple teams and weeks to resolve. The volume of these events was significant. Nobody had quantified it across the organisation because no single team owned the full picture.

Key Hypothesis Statements

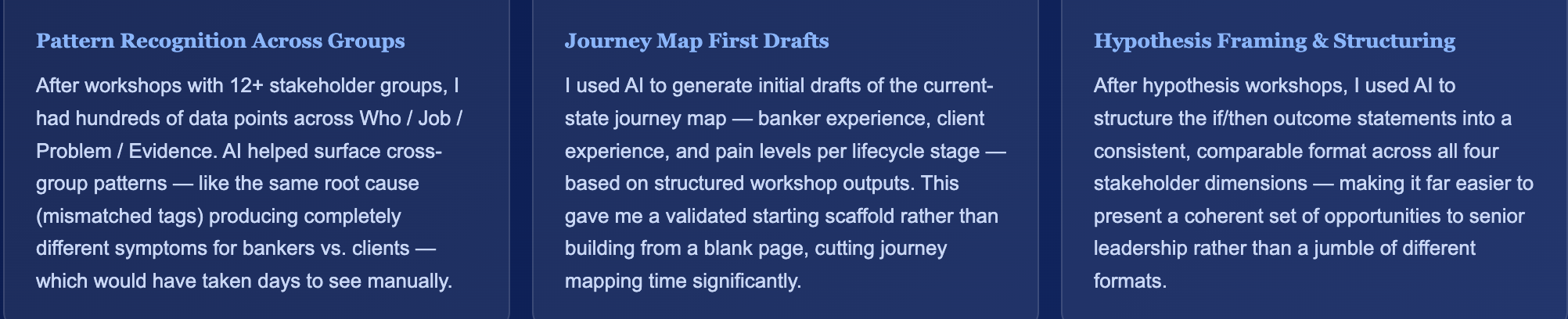

AI-Assisted Synthesis & Journey Drafting

Working smarter, not just faster

After each brainstorming workshop I had hundreds of sticky notes, verbatim inputs, and pattern threads to make sense of. I used AI - specifically Claude -as a synthesis partner to accelerate structure, draft journey frameworks, and surface patterns I could then validate and refine with stakeholders.

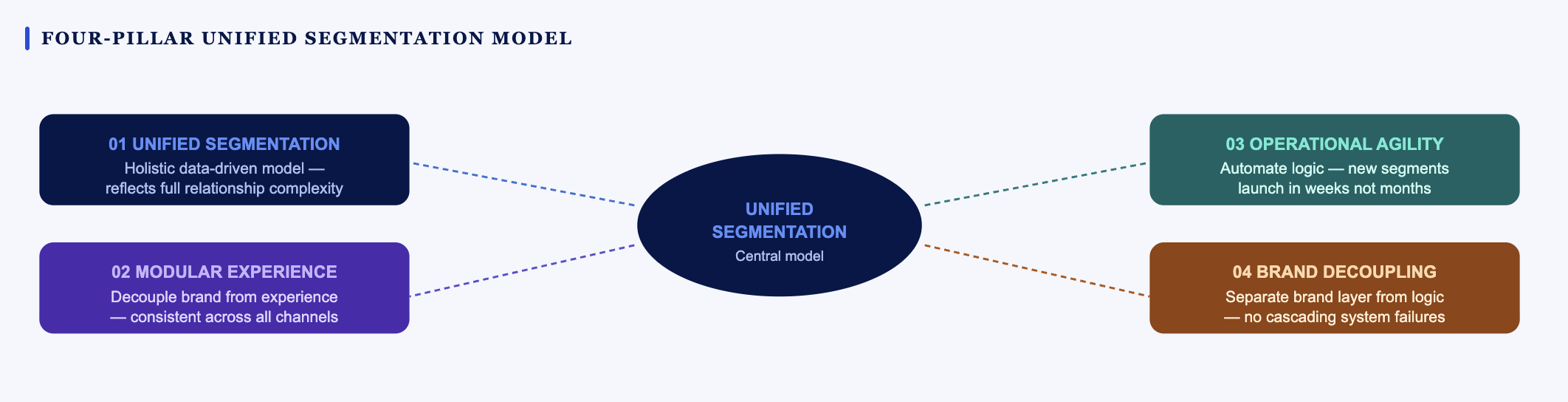

Based on discovery, synthesis, hypothesis workshops, and stakeholder alignment, I contributed to the Experience Objects framework - a strategic architecture designed to solve the segmentation problem at its root.

What an Experience Object is: A data construct that delivers consistent, context-aware experiences to customers across every channel. Instead of each product maintaining its own segmentation logic, a single Experience Object - calculated by Data & Analytics and stored in GCP - drives the experience across digital channels, communications, servicing, and human touchpoints simultaneously.

The three MVP attributes we defined for phase one:

Visual Branding - Theme and navigation adapt to the customer's program and sub-program. A Chase Private Client sees a different visual experience than a Starter customer, consistently across every surface.

Communication - Content and tone of voice calibrated to the customer's relationship level. Not generic messaging - contextual communication that reflects what JPMC actually knows about that customer.

Servicing - Support model matched to service tier. A JPMorgan Private Bank client reaches a dedicated relationship manager. A Starter customer reaches the right support channel for their needs. The routing is automatic and consistent.

The six design principles that governed the framework:

Context -acknowledge the full context of a customer's relationships, accounts, and preferences.

Cross-Channel - the experience transitions seamlessly between channels.

Trust - consistency in times of change and transition.

Intuitive - preemptively meet expectations before customers ask.

Connection - humanise interactions irrespective of channel.

Adaptable - meet changing organisational needs without rebuilding from scratch.

The persona-based interaction model means that as a customer's relationship with JPMC changes - new account, life event, business growth — the Experience Object updates and the digital experience adapts automatically. A customer who holds a Chase checking account, a JPMorgan investment account, and a business banking relationship sees all three coherently in one unified view — with the right service level, right visual branding, and right communication for each relationship simultaneously.

This was the vision I helped define and present to senior leadership. The implementation roadmap was handed off to engineering and product teams.

The framework contributed to a 20% reduction in process review cycles — measured over the period following the discovery and alignment work. This came from a specific design contribution: replacing fragmented per-team review processes with a shared service blueprint that all teams worked from. Fewer review loops. Clearer ownership. Less back-and-forth.

I want to be honest about what I can and cannot claim here. The Experience Objects architecture is a long-term programme. Implementation was ongoing at the time I was on this engagement. The 20% cycle reduction reflects the impact of the discovery and alignment work specifically — not the shipped product,

1

Branding

2

Development

3

Quick Support

4

Design Branding

5

UI/UX Design

1

Branding

2

Development

3

Quick Support

4

Design Branding

5

UI/UX Design

RELATED POSTS

Connect with me